Biz Community

Agriculture has long been both the strength and weakness of Morocco’s economy – strength in that it has been a driver of growth, a weakness because of its high volatility. The sector’s average growth rate fell from 10.6% between 1985 and 1991, to 0.27% between 1991 and 2004.

The volatility of the agriculture sector (deviations of output relative to its average) during this period, grew to become eight times higher than that of the Middle East and North Africa region (Morocco: the challenge of becoming an emerging economy, Coface).

Morocco has two key agricultural segments. The first is mainly concentrated in the irrigated areas that occupy 20% of the agricultural land used. The second is livestock, which employs the majority of the agricultural workforce and occupies 80% of farming land used. Morocco’s food-processing industry is relatively important and benefits from a strong agricultural base. With a population of 32 million and growing, the country is a major market for the region’s agricultural produce.

The Moroccan government has made the development of its agricultural sector a priority. Since the introduction of the ‘Green Morocco’ plan in 2008, agricultural productivity per worker has risen at a fast pace. Over the last five years, the agricultural growth rate has reached an average of 9.3%. Productivity per hectare has also grown, due to an increase in irrigated plots.

The Green Morocco plan has led to nearly 100 billion dirhams of investments in drainage systems over the last seven years and generated an additional GDP of 43 billion dirhams. Growth in the sector has improved significantly over the last seven years and the government’s goal of doubling agricultural GDP by 2020, therefore, seems achievable. Average annual growth of agricultural GDP reached 7.7% in 2015, exceeding 118 billion dirhams – compared to 75 billion in 2008.

Trade and investment

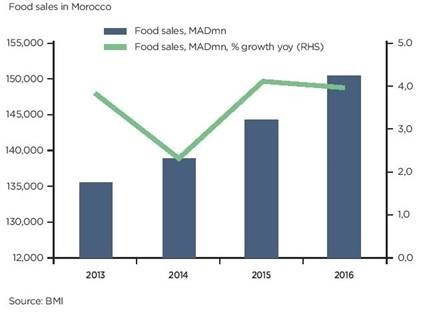

According to a study carried out by l’Office des Changes, food industry production and exports doubled in the period 2000-2013 (Etude sur l’industrie alimentaire au Maroc, 2015, Département des Statistiques des Echanges Extérieurs du Maroc). The share of food exports in total exports increased from 9.1% in 2011 to 11.2% in 2014. The EU accounts for 51.4% of Moroccan trade and its leading trading partners, Spain and France, account for over 55% of total trade with the EU.

Growth in the agribusiness has attracted more foreign investors to Morocco. Foreign direct investments rose to DH 10.2 billion in 2013, up from 531 million dirhams in 2010. The food sector’s share of FDI receipts in total foreign direct investment jumped from 1.5% in 2010 to 26.2% in 2013.

The structure of Morocco’s food exports has been relatively stable over the last 10 years. In 2014, 50% of food exports related to the fishing industry, 14% were fruit and vegetables and 8% meat. Based on the growth in agribusiness, supported by the government, the country has introduced new products such as meat processing and preparation, chocolate and confectionery products.

Further developments

Optimism in the sector has been bolstered by the government-initiated Green Morocco Plan, which also aims to reduce the industry’s weather-related production risks by 2020. A further programme, to update logistical frameworks, was initiated in 2010.

This programme should result in reduced transport costs and improved management and traceability of stocks. The sector itself is also working on developments and, between 2007 and 2012, climbed up 44 places in the Logistics Performance Index listing (LPI)3. The government’s twin strategies of producing high-yield, market-related agriculture, as well as improving the existing water conservation programme, could produce good results in the medium-to-long-term.

The biggest challenges and obstacles

The biggest challenge relates to the sector’s failure to bring added value. The development of agribusiness has been slow and accounts for only 5% of Moroccan GDP, compared to 15% for agriculture. Nevertheless, the sector has huge growth potential, as the demand for processed goods has been rising in line with the progressive transformation of consumption patterns over the last twenty years. In fact, the demand for agribusiness products has been growing at an average annual rate of 4% since 2004 (the same as the growth rate seen in household demand for agricultural products).

On the investment side, the use of production factors remains low. The use of fertiliser per hectare in Morocco is four times lower than in France, while mechanisation is eleven times lower than in Spain. In addition, farmers have little access to banking systems and only 18% are able to obtain bank loans which mean that project financing for agribusiness is limited.

Drought and irregular rainfall are among the sector’s most important obstacles to development, resulting in huge volatility in terms of agricultural output. The government is introducing measures to address this problem. A major public investment programme should make it possible to increase the amount of irrigated land and productivity per hectare, while crop conversion should enable the production of higher added value goods.

If current global economic conditions and depressed food prices continue, private investors will have little incentive to risk entering seemingly unprofitable businesses. A prolonged global economic downturn could harm the growth performance of countries in the region, reducing the revenues available for agricultural investment and development.

Government incentives and funding crucial

Government incentives are crucial for the development of Morocco’s agricultural activities. The Green Morocco Plan aims to mobilise 10 billion dirhams annually for the agricultural sector, by 2020. In this way, the lack of access to banking loans for farmers is partly compensated for by government incentives. Under the Green Morocco Plan, 70% to 80% of the funding for projects within ‘Pillar II’, will be supported by domestic or international investors. The remainder will be largely taken in charge by the agricultural development fund (FDA). The state provides financial aid for ‘Pillar I’ projects, in the form of grants and bonuses, through the FDA.

Overall, despite some obstacles, Morocco’s agribusiness shows very promising perspectives. Serious efforts by the government to address some of the issues could lead to a more fully integrated and efficient domestic supply chain. In addition, the country’s rising population and expanding GDP should lead to increased consumer demand for higher added value agricultural goods, further sustaining the agribusiness sector.